How voluntary supplemental health plans help employees cover medical costs

An unexpected medical bill is one of the biggest financial concerns many American workers face. A Kaiser Family Foundation poll shows more than half of U.S. adults (57%) are very or somewhat worried about being able to pay an unexpected medical bill, outweighing concerns about paying for housing, utilities, food or prescription medications. Perhaps more surprising is this concern isn’t limited to the uninsured. In fact, 42% of those with insurance say they’re worried about their ability to pay medical bills if they get sick or have an accident. Rising health care costs, reduced transparency in the care process, and lower personal savings combine to create potentially dangerous gaps in employees’ health and well-being.

And health care costs often extend far beyond doctor and hospital bills. Even the best major medical insurance can leave employees with significant out-of-pocket expenses for copayments and coinsurance in addition to noncovered expenses such as transportation or lodging for treatment, assistive devices, child care and other everyday bills that still need to be paid while employees miss work due to illness or injury.

Employers can help employees bridge this gap and protect their financial well-being by including voluntary supplemental coverage in their benefits packages.

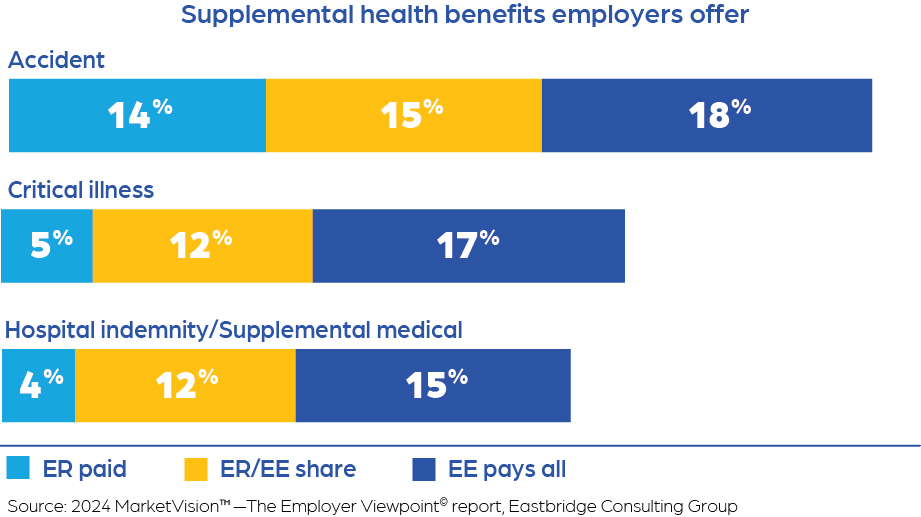

Benefits employers offer

Not surprisingly, employers continue to be most likely to offer medical, dental, prescription drug and vision insurance as either employer-paid, employer-employee share or employee-paid coverage, according to Eastbridge Consulting Group’s 2024 MarketVision™—The Employer Viewpoint© report. However, nearly half (47%) offer accident coverage and about a third offer critical illness (34%) or hospital indemnity/supplemental medical (31%).

Accident, critical illness and hospital indemnity/supplemental medical also are among the top 10 products employers offer as a voluntary benefit. And potential for these products is high: Hospital indemnity/supplemental medical and critical illness are both in the top three products ranked by sales potential index, which compares the percentage of employers that do not offer each product and the percentage interested in offering it on a voluntary basis.

Why employers offer voluntary

Addressing the financial well-being of employees is one of the most important factors employers cite when they decide to offer voluntary benefits, along with employee interest in the products, and helping recruit and retain employees. Eastbridge’s survey also shows improved employee well-being and improved financial protection from out-of-pocket medical costs are among the most important outcomes employers hope to achieve by offering voluntary benefits. Providing a safety net against rising medical costs has grown in importance in recent years, increasing 20% between 2022 and 2024.

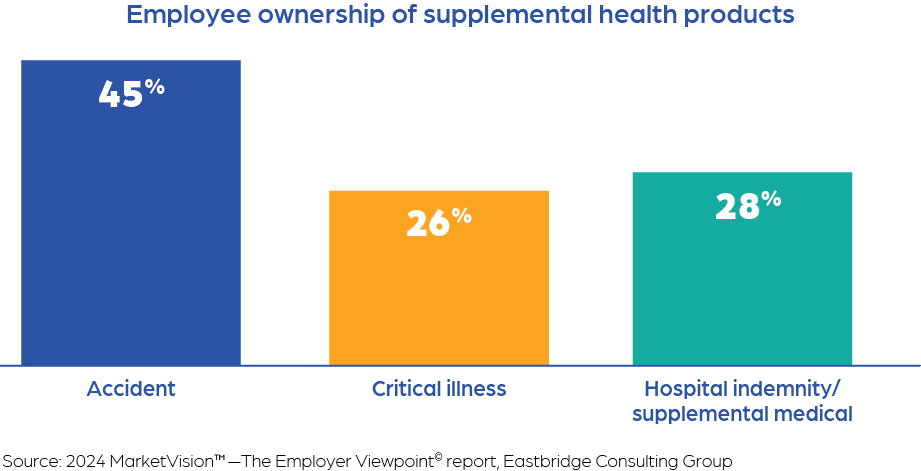

Employee interest in supplemental health coverage

Employee interest in and demand for additional financial protection benefits is driving growth in supplemental health products. Almost half of employees own accident coverage, and more than one-quarter own hospital indemnity/supplemental medical and critical illness products, according to Eastbridge’s 2025 MarketVision™—The Employee Viewpoint© report. And they’re willing to pay for this coverage: Accident is one of the top two products employees own on a voluntary basis.

Employees are less likely to own voluntary critical illness or hospital indemnity/supplemental medical plans — but both types of coverage rank in the top five products employees are most interested in purchasing, according to Eastbridge’s voluntary buying interest index. The index is calculated based on the percentage of employees who don’t own the product at all and the percentage interested in purchasing it on a voluntary basis.

Why employees buy voluntary coverage

There’s no denying price matters. Reasonable cost for the coverage is the top reason employees cite for buying voluntary benefits — meaning the premiums are affordable for the value these products deliver. But rating nearly as highly are two closely tied reasons: the products meet employees’ needs, and they help fill gaps in medical coverage.

Research shows employers and employees alike are concerned about the potential impact of unexpected medical bills and spiraling health care costs. Voluntary supplemental health benefits including hospital indemnity/supplemental medical, critical illness and accident coverage offer an affordable solution that can help provide the financial protection employees need.

5Star Life Insurance Company (5Star Life) is dedicated to a collaborative experience with brokers and employers to meet the needs of today’s workforce with benefits solutions and a consumer experience that is second to none. Discover more about 5Star Life, our products and services, and our commitment to partnering with you by visiting us at 5starlifeinsurance.com.

Source: Kaiser Family Foundation analysis of National Health Interview Survey (NHIS) data, 2024 MarketVision™—The Employer Viewpoint© report, Eastbridge Consulting Group, 2025 MarketVision™—The Employee Viewpoint© report, Eastbridge Consulting Group

Products, benefits and options continue expanding to meet employer and employee needs

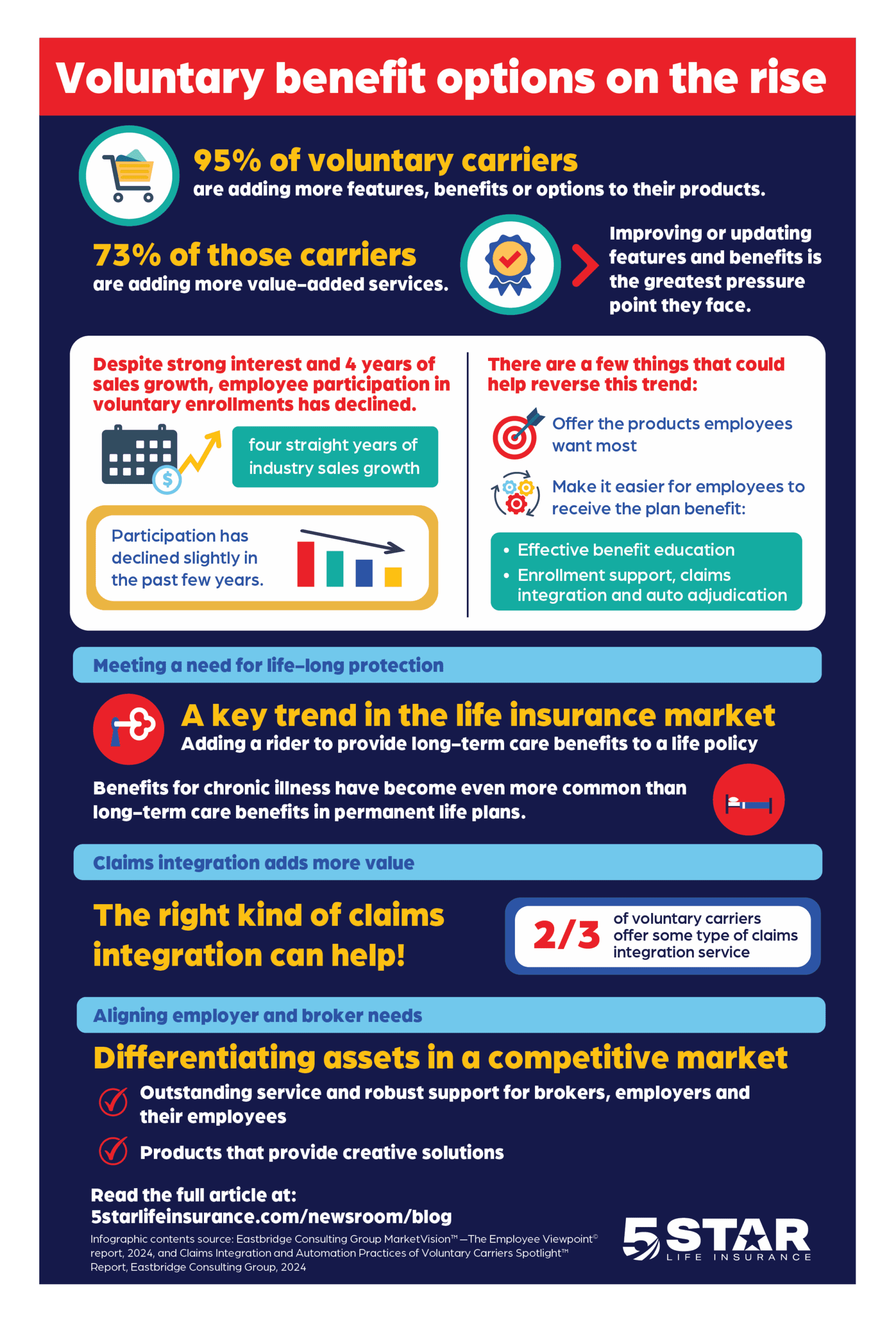

Employers and employees have access to an ever-increasing array of voluntary products with better benefits and greater options. Recent research shows virtually all (95%) voluntary carriers are adding more features, benefits or options to their products, and the majority (73%) are adding more value-added services.1 In fact, carriers surveyed say improving or updating features and benefits is the greatest pressure point they face with their voluntary products, and a strong majority of carrier feedback indicates brokers and producers are the main source of that pressure to innovate.

Despite significant employee interest in many types of voluntary benefits — not to mention four straight years of industry sales growth — participation in voluntary enrollments has declined slightly in the past few years. Participation in supplemental health products such as hospitalization, critical illness and accident coverage averages 16%, while participation in permanent life is even lower, primarily driven by the overall complexity of that product.3 Offering products employees want most — and making it easier for employees to receive the benefits of these plans through more effective benefit education and enrollment support, claims integration and auto adjudication — could help reverse this trend.

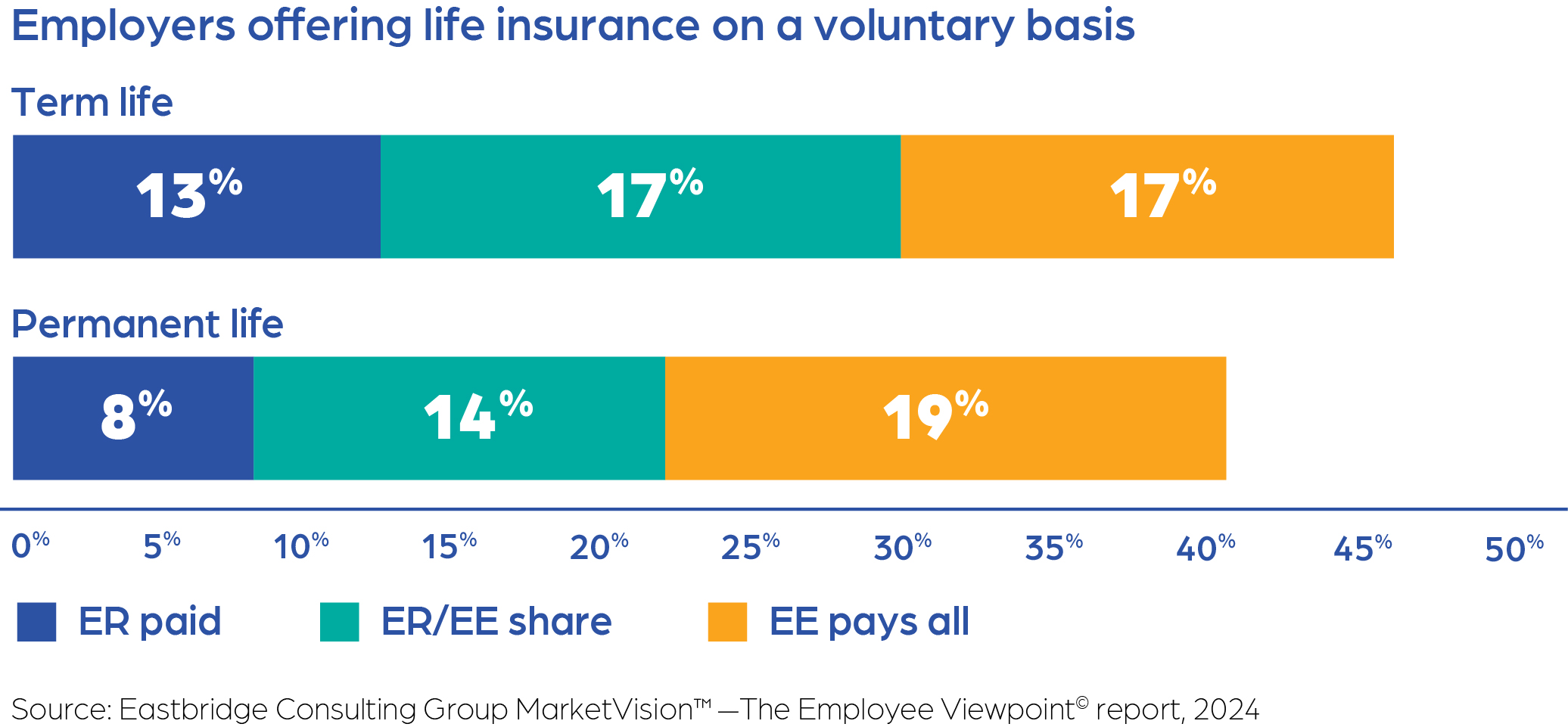

Meeting a need for life-long protection

Both employers and employees clearly see the value of life insurance: Research shows life insurance is among the voluntary products employers are most likely to offer, with slightly more now offering permanent life (19%) than term life (17%). Life insurance also is the coverage employees are most likely to own on a voluntary basis: 16% own permanent life and 12% own term life. While awareness of lifelong financial protection is on the rise, only 41% of employers currently offer permanent life insurance—whether fully employer-funded, cost-shared, or entirely employee-paid.2 Even fewer extend benefits that help offset expenses associated with long-term care, including support for cognitive impairments or physical limitations. A key trend in the life insurance market is combining both types of coverage by adding a rider to provide long-term care benefits to a life policy, which is typically more cost-effective for employees than stand-alone long-term care coverage.

About half the plans profiled in a new Eastbridge study offer an optional rider that addresses this need on their permanent life products.3 These riders typically advance the policy’s death benefit in monthly benefit amounts to pay for long-term care/assistive services provided in a facility or at home. Premiums for the life policy are waived while the insured receives benefits under this acceleration. Whether triggered by facility confinement for long-term care or home health care, benefits for chronic illness have become even more common than long-term care benefits in permanent life plans. Carriers surveyed say interest in both long-term care and chronic illness benefits are trends they expect to see continuing in the future, despite the additional complexity they create for administrative and claims systems.

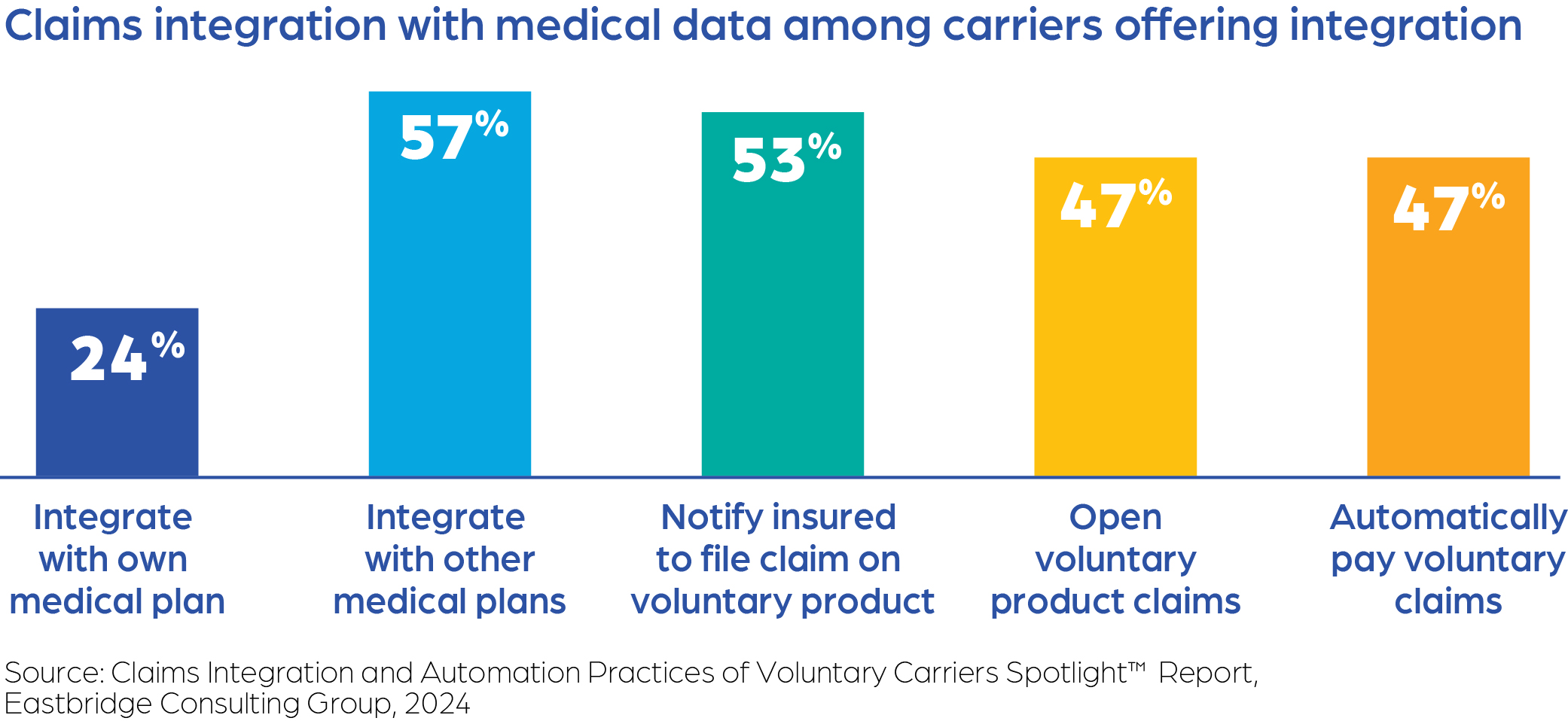

Claims integration adds more value

Claims integration is another fast-growing trend with expanding capabilities. Research shows more than two-thirds of voluntary carriers offer some type of claims integration service.4 While the approach carriers take to provide this service varies, the majority of carriers offering claims integration will notify employees they should consider filing a voluntary claim, and nearly half automatically pay a voluntary claim for employees. Most carriers provide these services without an additional charge.

Aligning employer and broker needs

Brokers who want to help clients create the most effective — and most affordable — benefits package may need to beware of a tipping point. Carriers surveyed for Eastbridge’s Product Trends report1 say their biggest challenges include balancing the demand for richer benefits with overall profitability and the need for affordable and simpler, easier-to-understand products. Benefits communication remains essential for a successful offering, but access to employees is a growing concern with the trend toward online self-enrollment. As this trend continues, employers and even brokers may need better education about the value of voluntary benefits and how an impactful communication process is a vital part of the offering.

Outstanding service that offers robust support for brokers, employers and their employees is increasingly recognized as a crucial and valuable asset in a competitive market. 5Star Life’s dedication to making this collaborative experience productive and rewarding sets us apart. Discover more about 5Star Life Insurance Company, our commitment to partnering with you, and our award-winning service recognized by Forbes two years in a row by visiting us at 5starlifeinsurance.com.

1 Voluntary Products Trends Frontline™ Report, Eastbridge Consulting Group, February 2024

2 MarketVision™—The Employer Viewpoint© Report, Eastbridge Consulting Group, February 2024

3 Voluntary Whole and Universal Life Products” Spotlight™ Report, Eastbridge Consulting Group, 2025

4 Claims Integration and Automation Practices of Voluntary Carriers Spotlight™ Report, Eastbridge Consulting Group, 2024

Excellent service can be a key differentiator in a competitive market

The voluntary benefits market is becoming increasingly crowded and competitive — and with so many carriers in the industry, it can be difficult to differentiate based on products alone. A strong, comprehensive portfolio is still important, but a quickly growing aspect of the employee benefits industry is emerging as a key differentiator: service. Excellent service can make or break a carrier’s relationship with its broker and employer clients. Recent research by Eastbridge Consulting Group shows administration and service is among the top two most important criteria both brokers and employers use to select a voluntary carrier. also pop up on the lists for brokers and employers, including claims integration, billing options, integration with enrollment needs and online services.

In fact, service issues are overwhelmingly the number one reason brokers switch their top carriers, cited by 56% of brokers in a recent Eastbridge survey (and more than a third of brokers have changed their top three voluntary/worksite carriers in the past one to three years). Again, other issues aside from products or price emerge as primary reasons for this turnover, including better integration with a client’s enrollment or administrative needs, good claims management and better online services. Here are three key areas brokers should consider when choosing and working with carriers to best meet their — and their clients’ — expectations for excellent service.

Administration

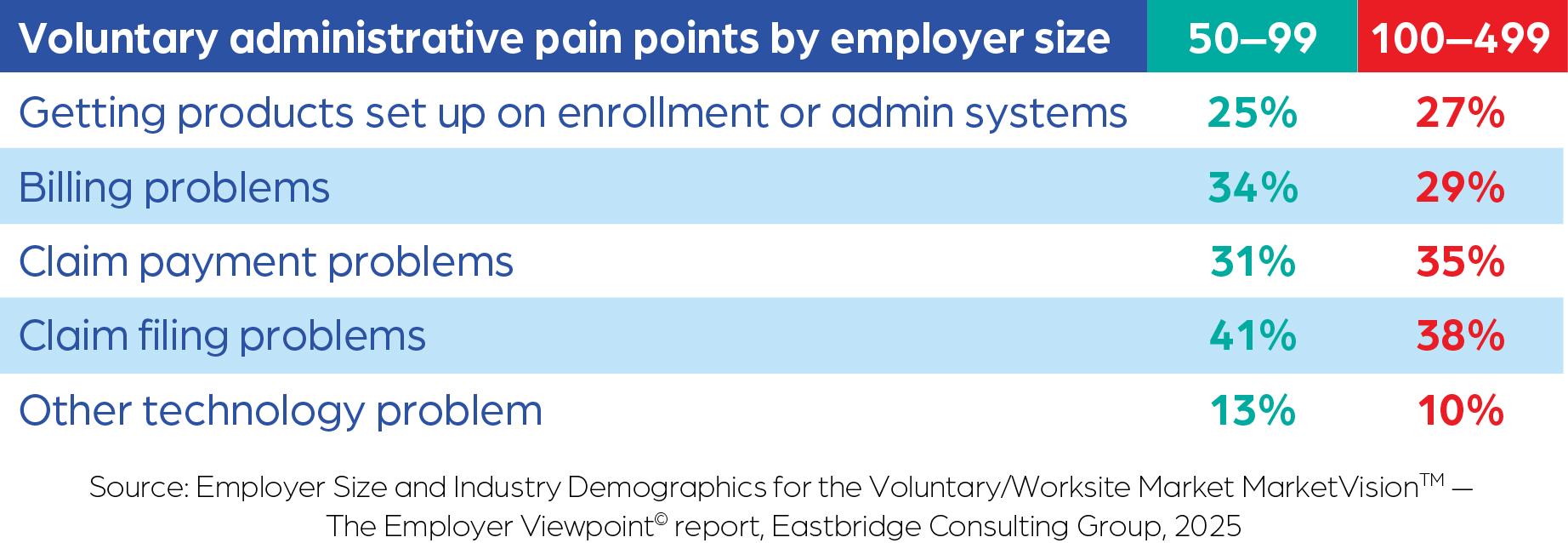

Brokers can help ensure their clients get strong support with benefits administration by understanding where they experience the most trouble. Getting products set up on enrollment and benefits administration systems and claims payment problems cause the most voluntary administration difficulty for employers, according to Eastbridge’s MarketVisionTM — The Employer Viewpoint© report. This is especially true for employers in manufacturing, the qa sector most likely to cite billing problems as an administrative issue. Health care employers also tend to list several administrative issues: a third or more say claims filing and payment, billing, and getting products set up on enrollment or benefit administration systems are administrative pain points, and more than one-quarter say electronic data exchange is the primary cause of billing problems.

Large employers are most likely to indicate they have numerous problems with benefits administration, but smaller employers with between 50 and 500 workers aren’t exempt from these concerns, and in many cases experience them more often than the overall average. Brokers and employers need to trust their carrier is as dedicated as they are to selecting the best enrollment and administrative support solutions. The right partner with the right tools and commitment is often the difference between a successful long-term relationship or a much shorter and less satisfying one.

Billing

The ability to access a wide range of capabilities and services online through a website or portal is essential to brokers, employers and employees. In fact, one-third of carriers surveyed for Eastbridge’s MarketVisionTM — The Employer Viewpoint© report say they wouldn’t choose a voluntary carrier that didn’t provide online administration, up from 21% just two years ago. Personal services employers are even more emphatic: 56% say they wouldn’t select a carrier without online administration services. Only 4% of employers don’t think this is important.

Online services

The ability to access a wide range of capabilities and services online through a website or portal is essential to brokers, employers and employees. In fact, one-third of carriers surveyed for Eastbridge’s MarketVisionTM — The Employer Viewpoint© report say they wouldn’t choose a voluntary carrier that didn’t provide online administration, up from 21% just two years ago. Personal services employers are even more emphatic: 56% say they wouldn’t select a carrier without online administration services. Only 4% of employers don’t think this is important.

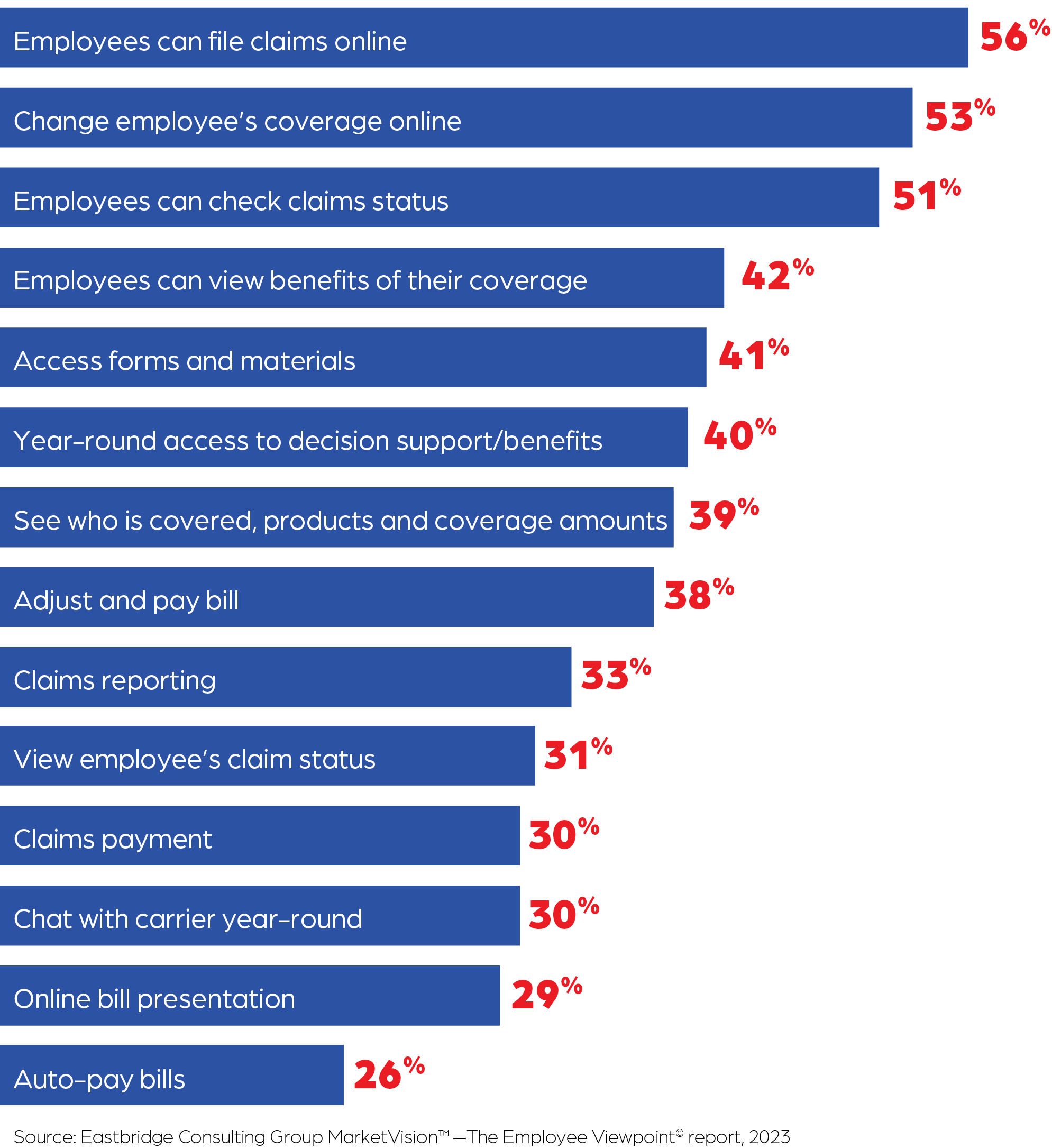

Employers check a long list of online services they consider critical. The top five are all employee-focused services, including the ability of employees to file claims, the ability to change employee’s coverages, the ability of employees to check their claim status, the ability of employees to view available benefits specific to their purchase, and the availability of forms and materials. Employers with 100–500 workers are among those placing the greatest emphasis on employees’ ability to file claims and check claim status.

Outstanding service that offers robust support for brokers, employers and their employees is increasingly recognized as a crucial and valuable asset in a competitive market. 5Star Life’s dedication to making this collaborative experience productive and rewarding sets us apart. Discover more about 5Star Life Insurance Company, our commitment to partnering with you, and our award-winning service recognized by Forbes two years in a row by visiting us at 5starlifeinsurance.com.

Brokers use product bundling to offer clients more value

The best employee benefits package isn’t necessarily the one with the most bells and whistles. It’s the one the most employees sign up for — and the choice to participate often depends on a strong benefits education and enrollment support plan that empowers employees to make informed decisions.

Voluntary benefits complement and help fill the gaps in major medical coverage with benefits employees can use for copayments, deductibles or other out-of-pocket expenses when an accident or illness occurs. These unexpected costs can be sizeable, especially with the continuing trend toward high-deductible health plans. Brokers can help their clients incorporate voluntary benefits to design a comprehensive, affordable benefits plan that meets the unique needs of their workforce and attracts and retains top talent — but if employees don’t participate in it, the employer’s investment of valuable resources is wasted. That’s why any successful benefits package needs to involve more than products and rates. It also must focus on helping employees understand their options, see how the benefits available address their unique needs, and encourage them to actively participate in their benefits program. Brokers can help their clients leverage best-in-class technology and benefit communication strategies to drive stronger participation in their voluntary benefits.

Carriers offer flexibility and cost savings with product bundles

The number of carriers offering product bundles has grown significantly in the past four years. Eastbridge’s recent “Voluntary Product Trends” Frontline™ report shows more than a third of voluntary carriers now offer some type of bundle, most often supplemental health products such as accident, critical illness or hospital indemnity bundled with either core group disability and life products or medical and dental products.

Flexibility is a high priority for most carriers. These product bundles are more likely to be informal rather than fixed, so employees can select the products they want to purchase. Only one in five carriers that offer bundles present a set package where employees must make a yes or no election and can’t choose the components or coverage levels they need.

Carriers also understand the importance of helping employers create cost-effective benefits plans. Many carriers that bundle products offer premium discounts based on case demographics, risk and the types of products offered, such as medical plans, nonmedical employer-funded products or voluntary products. However, product quality and easier administration far outweigh price discounts for most brokers when choosing voluntary partners.

Product bundling meets employers’ top criteria for carrier selection

Product bundling can also play a role when employers select a voluntary carrier — but brokers may need to help connect the dots for their clients to see why. Recent Eastbridge research shows the top factors most important to employers when choosing a voluntary carrier are the price/value of the products offered and the ease of administration for billing and service. In addition, nearly two-thirds of employers say single billing for all voluntary products is an important or very important factor. These criteria all align precisely with the advantages of product bundling.

Packaging a better benefits plan

Brokers increasingly see the value in bundling voluntary products with one carrier to save their clients time and money through streamlined issue, billing and service, while carriers are meeting the demand for bundled products with flexibly designed packages. Together, brokers and carriers are helping employers achieve their goals for stronger value and easier administration — ultimately creating more competitive and affordable benefits packages for their employees. Voluntary product bundling appears to be both a growing trend and a winning strategy for all key stakeholders.

5Star Life Insurance Company is available to partner with brokers interested in helping their clients take advantage of the market’s trend toward product bundling. Learn more about us and our commitment to partnering with you and your clients by visiting us online.

The best employee benefits package isn’t necessarily the one with the most bells and whistles. It’s the one the most employees sign up for — and the choice to participate often depends on a strong benefits education and enrollment support plan that empowers employees to make informed decisions.

Voluntary benefits complement and help fill the gaps in major medical coverage with benefits employees can use for copayments, deductibles or other out-of-pocket expenses when an accident or illness occurs. These unexpected costs can be sizeable, especially with the continuing trend toward high-deductible health plans. Brokers can help their clients incorporate voluntary benefits to design a comprehensive, affordable benefits plan that meets the unique needs of their workforce and attracts and retains top talent — but if employees don’t participate in it, the employer’s investment of valuable resources is wasted. That’s why any successful benefits package needs to involve more than products and rates. It also must focus on helping employees understand their options, see how the benefits available address their unique needs, and encourage them to actively participate in their benefits program. Brokers can help their clients leverage best-in-class technology and benefit communication strategies to drive stronger participation in their voluntary benefits.

Communicate, communicate, communicate

Employees won’t sign up for benefits if they don’t understand where they might have gaps in their coverage, what benefits are available to them, and how those benefits can help protect them and their families — and nearly every plan has variations. That’s why effective benefits communication starts long before the planned enrollment period.

Brokers should consult with their clients to map out a communication and engagement plan starting at least one to two months before the enrollment. It’s important to use a variety of formats and methods to reach employees when and where they want: email, texts, website or intranet, print materials distributed at the office or mailed to employees’ homes, mobile apps, videos, and in-person or virtual meetings. The content should cover the benefits available, how they work and what they can provide. Claims scenarios that illustrate the value of the benefits and decision-support tools that guide employees in determining their coverage needs also are helpful.

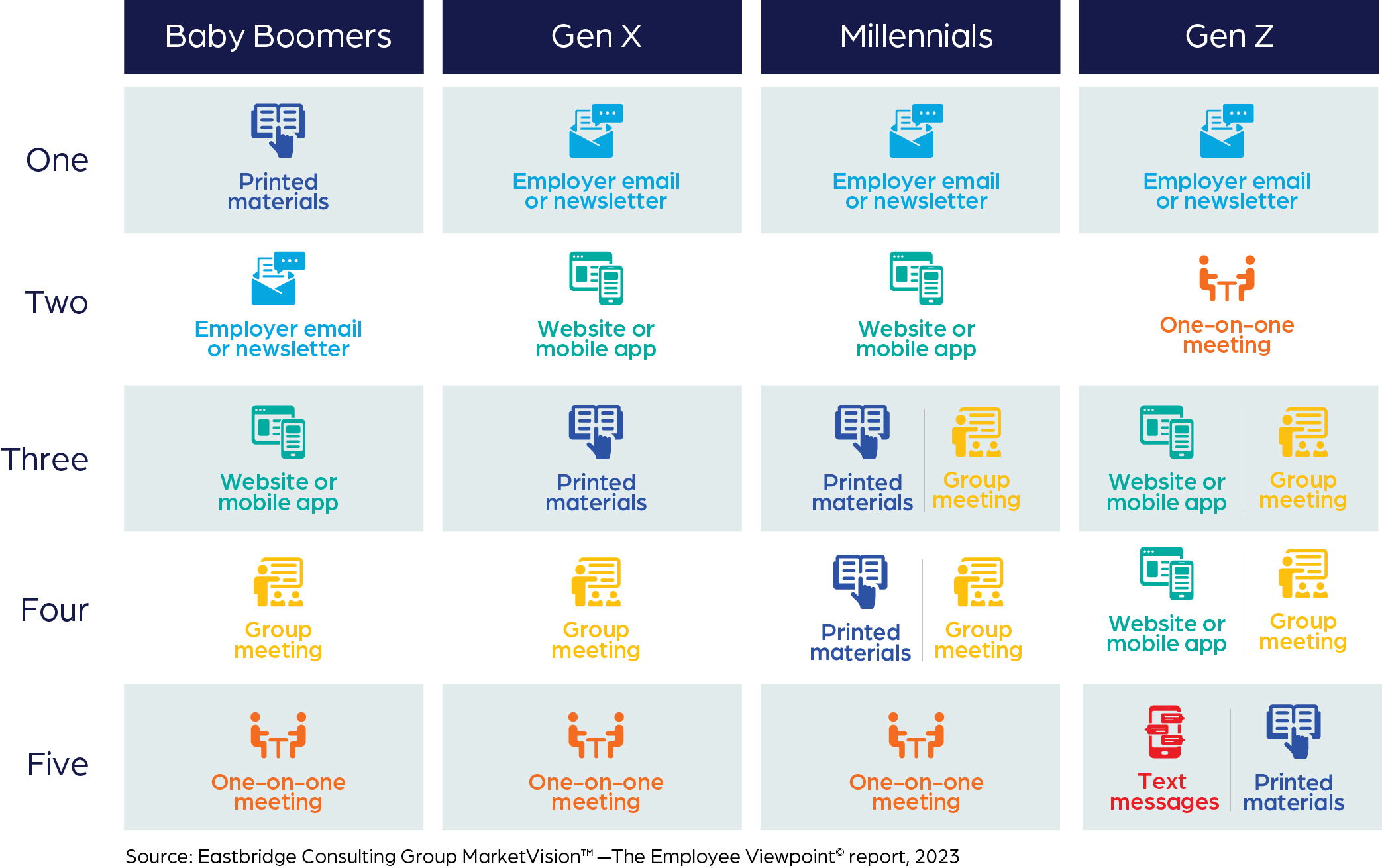

Customized, personalized communications based on an employee’s life stage can help increase employees’ understanding and engagement. A young single, a married 30-something with children, and a mature employee nearing retirement have different needs and communication preferences. For example, research shows Baby Boomers are much more likely than workers in other generations to find printed materials sent to them at home or at work helpful for introducing voluntary benefits, while text messages appeal more to Generation Z employees than to other workers. Benefit fairs and videos or webinars are among the least-preferred methods for all generations. Bottom line: Employees of all generations crave easy-to-understand content that helps them choose the best options for them.

Tap into technology

Using the right benefits administration platform can save time and money through faster product set-up and integration with other systems. Brokers should be sure the platform they choose can integrate with their clients’ payroll and HRIS systems through file exchange or application programming interface technology. In addition to these critical integrations, employers also expect access to tools that enable alternative premium remittance while still remaining on a list bill environment, including automated clearinghouse debit and credit.

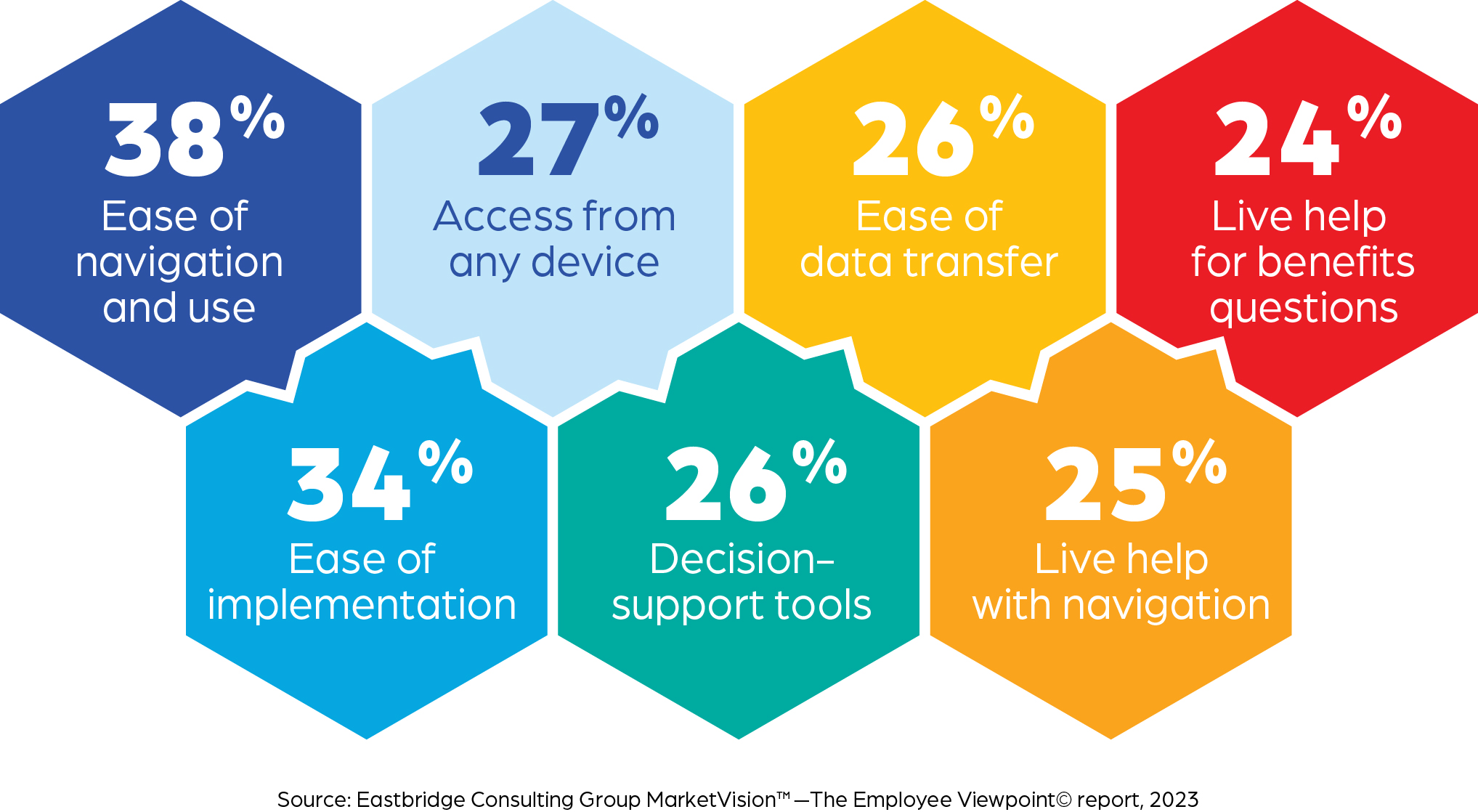

Brokers can build stronger consulting relationships with their clients by helping them choose the technology that best meets their needs. An Eastbridge Consulting Group survey* of more than 1,000 employers shows ease of navigation and use and ease of implementation are the most important factors they consider when choosing a voluntary enrollment platform. The ability to access and enroll in benefits from any device such as a laptop, tablet or phone; availability of decision-support tools and benefits education; ease of data transfer after the enrollment, and access to a live person to help them navigate through the system or to ask questions about the benefits offered are other key capabilities employers look for.

Brokers may be better positioned to provide the most effective technology platforms with support from their carrier partners for appropriate tech fees and commissions. 5Star Life Insurance Company (5Star Life) partners with brokers and their clients to develop a mutually beneficial solution that provides the necessary human resource management tools while offering employees a meaningful and engaging experience to help make informed decisions.

Keep enrollment active — and personal

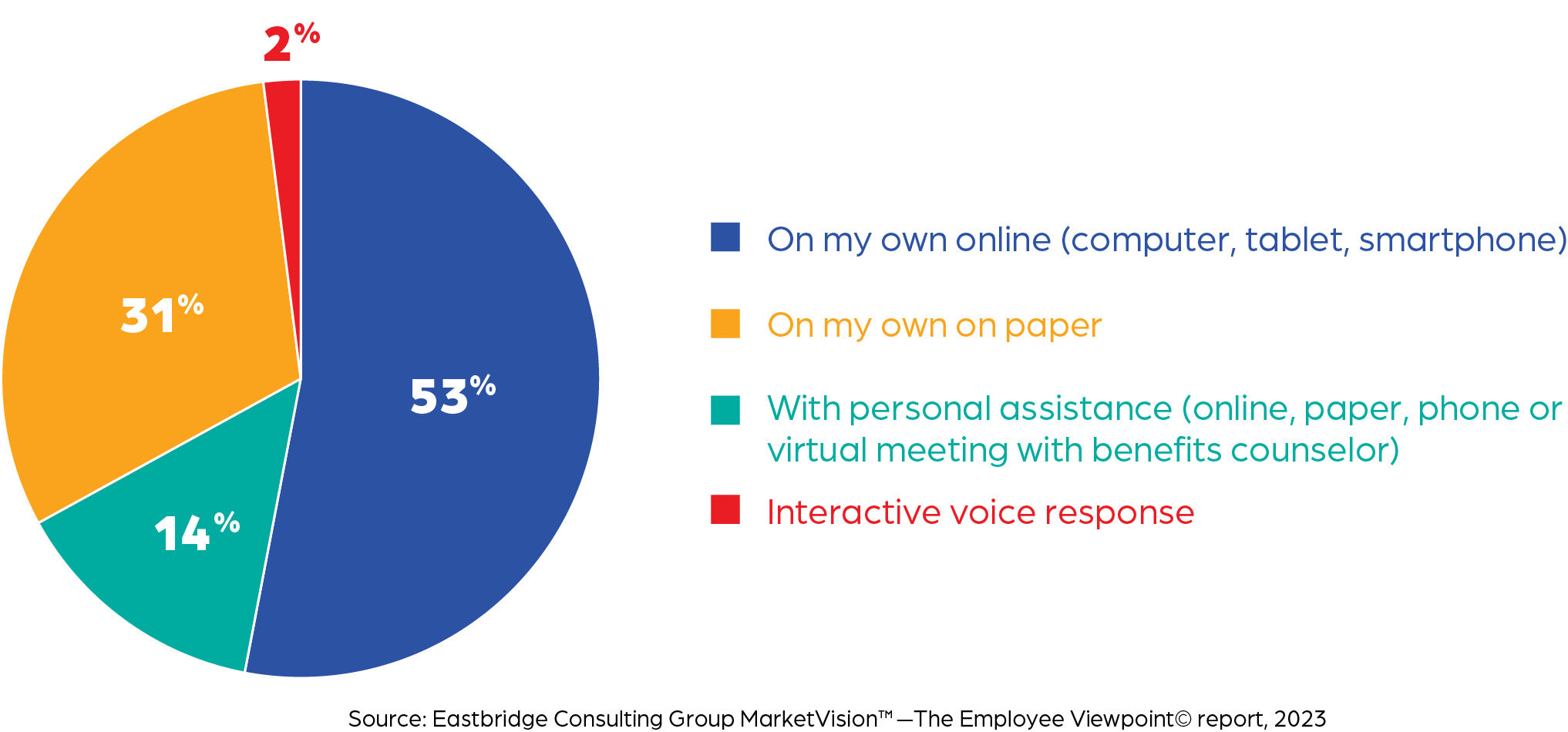

Technology is an invaluable tool to help drive enrollment participation, but high-tech is most effective when balanced with high-touch. The market is gravitating toward online, self-service enrollments, but that could mean a significant number of employees aren’t getting the personal support they need to understand their benefits options and help them make important decisions that affect their and their families’ health and financial security. Most voluntary benefits carriers agree enroller-assisted enrollments — face-to-face or virtual — tend to drive the highest participation. As with communication, best practice is to use a variety of enrollment methods accessible when, where and how employees want.

Research also shows greater adoption of voluntary benefits when they’re enrolled on the same system and at the same time as other benefits, rather than offered off-cycle. These coverages also gain more traction when they’re placed in the enrollment system immediately following core benefits such as major medical coverage. Active enrollments are another best practice to encourage to ensure employees take time to review and make a conscious decision on each benefit option.

5Star Life is available to partner with brokers interested in helping their clients drive stronger benefits participation with enhanced communication, robust technology solutions and effective enrollment practices. Learn more about us and our commitment to making your clients’ open enrollments as successful as possible by visiting us at 5Star Life .