How voluntary supplemental health plans help employees cover medical costs

An unexpected medical bill is one of the biggest financial concerns many American workers face. A Kaiser Family Foundation poll shows more than half of U.S. adults (57%) are very or somewhat worried about being able to pay an unexpected medical bill, outweighing concerns about paying for housing, utilities, food or prescription medications. Perhaps more surprising is this concern isn’t limited to the uninsured. In fact, 42% of those with insurance say they’re worried about their ability to pay medical bills if they get sick or have an accident. Rising health care costs, reduced transparency in the care process, and lower personal savings combine to create potentially dangerous gaps in employees’ health and well-being.

And health care costs often extend far beyond doctor and hospital bills. Even the best major medical insurance can leave employees with significant out-of-pocket expenses for copayments and coinsurance in addition to noncovered expenses such as transportation or lodging for treatment, assistive devices, child care and other everyday bills that still need to be paid while employees miss work due to illness or injury.

Employers can help employees bridge this gap and protect their financial well-being by including voluntary supplemental coverage in their benefits packages.

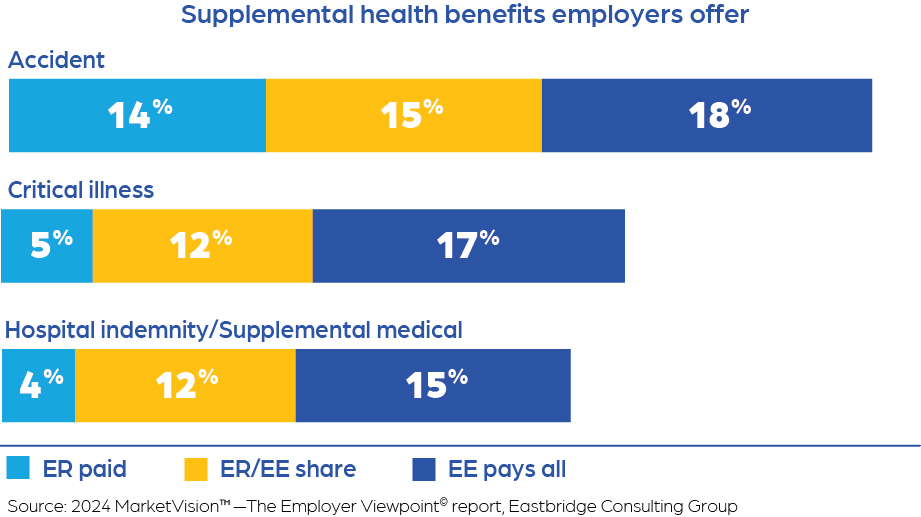

Benefits employers offer

Not surprisingly, employers continue to be most likely to offer medical, dental, prescription drug and vision insurance as either employer-paid, employer-employee share or employee-paid coverage, according to Eastbridge Consulting Group’s 2024 MarketVision™—The Employer Viewpoint© report. However, nearly half (47%) offer accident coverage and about a third offer critical illness (34%) or hospital indemnity/supplemental medical (31%).

Accident, critical illness and hospital indemnity/supplemental medical also are among the top 10 products employers offer as a voluntary benefit. And potential for these products is high: Hospital indemnity/supplemental medical and critical illness are both in the top three products ranked by sales potential index, which compares the percentage of employers that do not offer each product and the percentage interested in offering it on a voluntary basis.

Why employers offer voluntary

Addressing the financial well-being of employees is one of the most important factors employers cite when they decide to offer voluntary benefits, along with employee interest in the products, and helping recruit and retain employees. Eastbridge’s survey also shows improved employee well-being and improved financial protection from out-of-pocket medical costs are among the most important outcomes employers hope to achieve by offering voluntary benefits. Providing a safety net against rising medical costs has grown in importance in recent years, increasing 20% between 2022 and 2024.

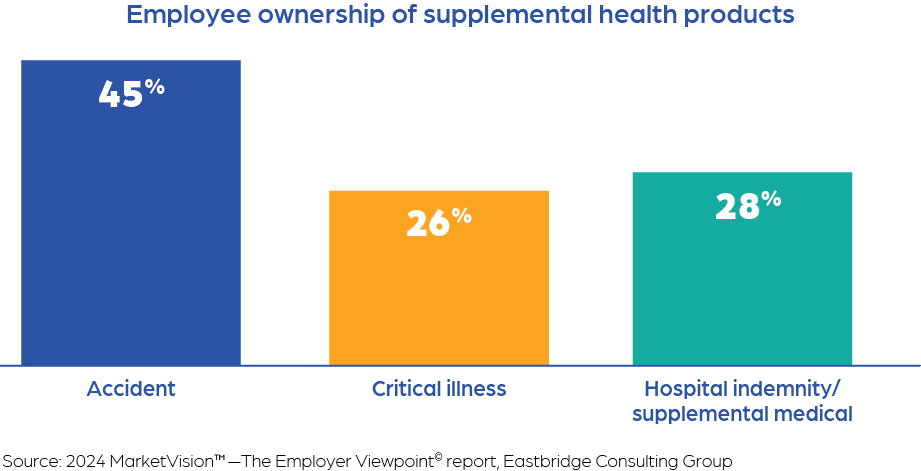

Employee interest in supplemental health coverage

Employee interest in and demand for additional financial protection benefits is driving growth in supplemental health products. Almost half of employees own accident coverage, and more than one-quarter own hospital indemnity/supplemental medical and critical illness products, according to Eastbridge’s 2025 MarketVision™—The Employee Viewpoint© report. And they’re willing to pay for this coverage: Accident is one of the top two products employees own on a voluntary basis.

Employees are less likely to own voluntary critical illness or hospital indemnity/supplemental medical plans — but both types of coverage rank in the top five products employees are most interested in purchasing, according to Eastbridge’s voluntary buying interest index. The index is calculated based on the percentage of employees who don’t own the product at all and the percentage interested in purchasing it on a voluntary basis.

Why employees buy voluntary coverage

There’s no denying price matters. Reasonable cost for the coverage is the top reason employees cite for buying voluntary benefits — meaning the premiums are affordable for the value these products deliver. But rating nearly as highly are two closely tied reasons: the products meet employees’ needs, and they help fill gaps in medical coverage.

Research shows employers and employees alike are concerned about the potential impact of unexpected medical bills and spiraling health care costs. Voluntary supplemental health benefits including hospital indemnity/supplemental medical, critical illness and accident coverage offer an affordable solution that can help provide the financial protection employees need.

5Star Life Insurance Company (5Star Life) is dedicated to a collaborative experience with brokers and employers to meet the needs of today’s workforce with benefits solutions and a consumer experience that is second to none. Discover more about 5Star Life, our products and services, and our commitment to partnering with you by visiting us at 5starlifeinsurance.com.

Source: Kaiser Family Foundation analysis of National Health Interview Survey (NHIS) data, 2024 MarketVision™—The Employer Viewpoint© report, Eastbridge Consulting Group, 2025 MarketVision™—The Employee Viewpoint© report, Eastbridge Consulting Group

Empowering Brokers

Stay ahead of the curve! Sign up below to receive our exclusive Thought Leadership Series articles and gain the latest insights and expert tips. Don’t miss out — click the link to explore even more valuable content that can elevate your knowledge.