Products, benefits and options continue expanding to meet employer and employee needs

Employers and employees have access to an ever-increasing array of voluntary products with better benefits and greater options. Recent research shows virtually all (95%) voluntary carriers are adding more features, benefits or options to their products, and the majority (73%) are adding more value-added services.1 In fact, carriers surveyed say improving or updating features and benefits is the greatest pressure point they face with their voluntary products, and a strong majority of carrier feedback indicates brokers and producers are the main source of that pressure to innovate.

Despite significant employee interest in many types of voluntary benefits — not to mention four straight years of industry sales growth — participation in voluntary enrollments has declined slightly in the past few years. Participation in supplemental health products such as hospitalization, critical illness and accident coverage averages 16%, while participation in permanent life is even lower, primarily driven by the overall complexity of that product.3 Offering products employees want most — and making it easier for employees to receive the benefits of these plans through more effective benefit education and enrollment support, claims integration and auto adjudication — could help reverse this trend.

Meeting a need for life-long protection

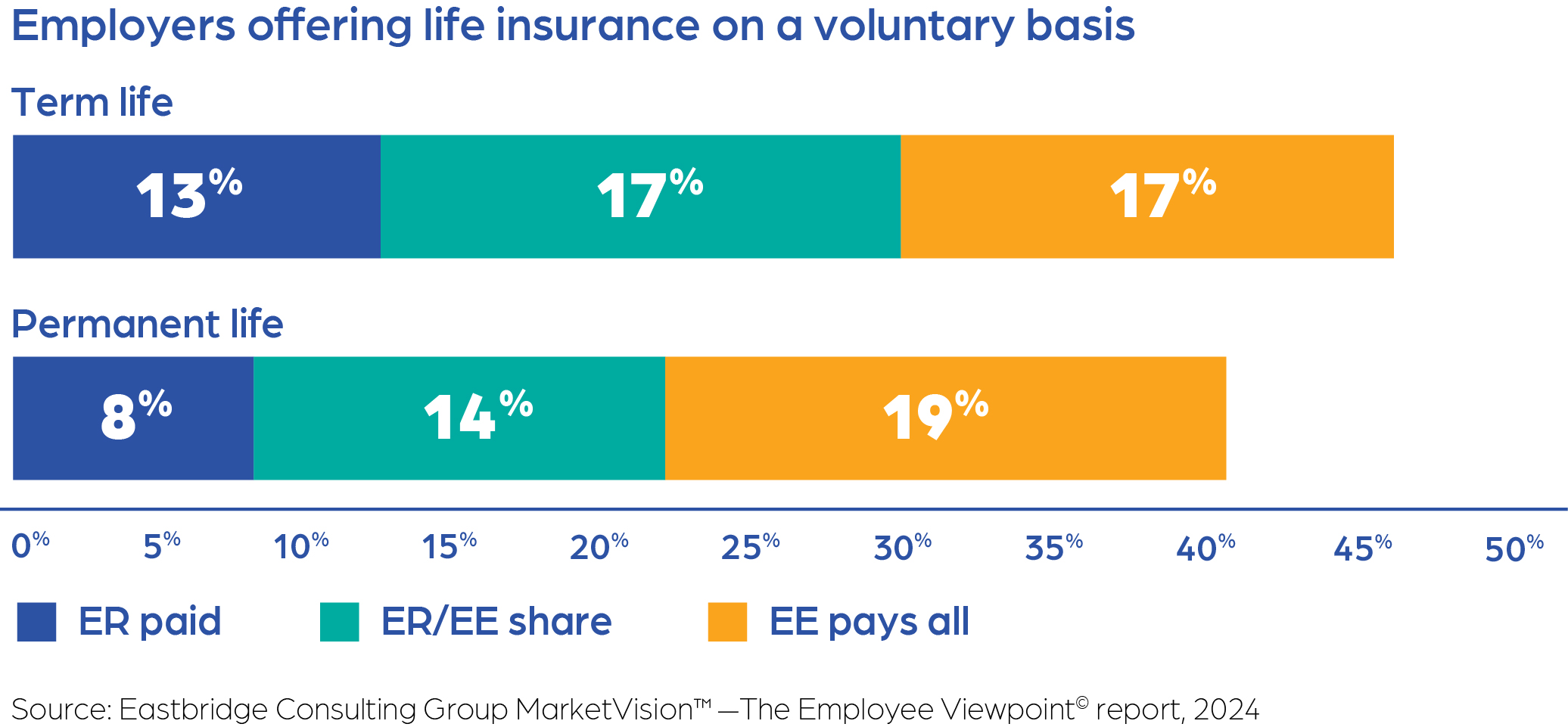

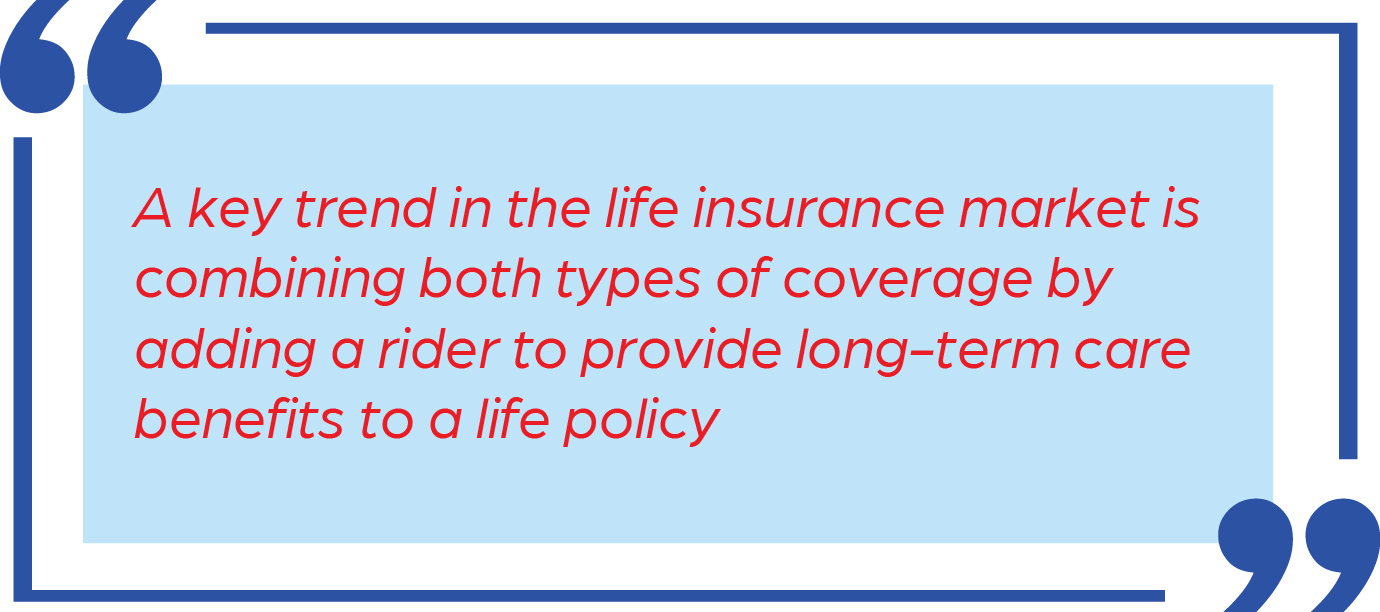

Both employers and employees clearly see the value of life insurance: Research shows life insurance is among the voluntary products employers are most likely to offer, with slightly more now offering permanent life (19%) than term life (17%). Life insurance also is the coverage employees are most likely to own on a voluntary basis: 16% own permanent life and 12% own term life. While awareness of lifelong financial protection is on the rise, only 41% of employers currently offer permanent life insurance—whether fully employer-funded, cost-shared, or entirely employee-paid.2 Even fewer extend benefits that help offset expenses associated with long-term care, including support for cognitive impairments or physical limitations. A key trend in the life insurance market is combining both types of coverage by adding a rider to provide long-term care benefits to a life policy, which is typically more cost-effective for employees than stand-alone long-term care coverage.

About half the plans profiled in a new Eastbridge study offer an optional rider that addresses this need on their permanent life products.3 These riders typically advance the policy’s death benefit in monthly benefit amounts to pay for long-term care/assistive services provided in a facility or at home. Premiums for the life policy are waived while the insured receives benefits under this acceleration. Whether triggered by facility confinement for long-term care or home health care, benefits for chronic illness have become even more common than long-term care benefits in permanent life plans. Carriers surveyed say interest in both long-term care and chronic illness benefits are trends they expect to see continuing in the future, despite the additional complexity they create for administrative and claims systems.

Claims integration adds more value

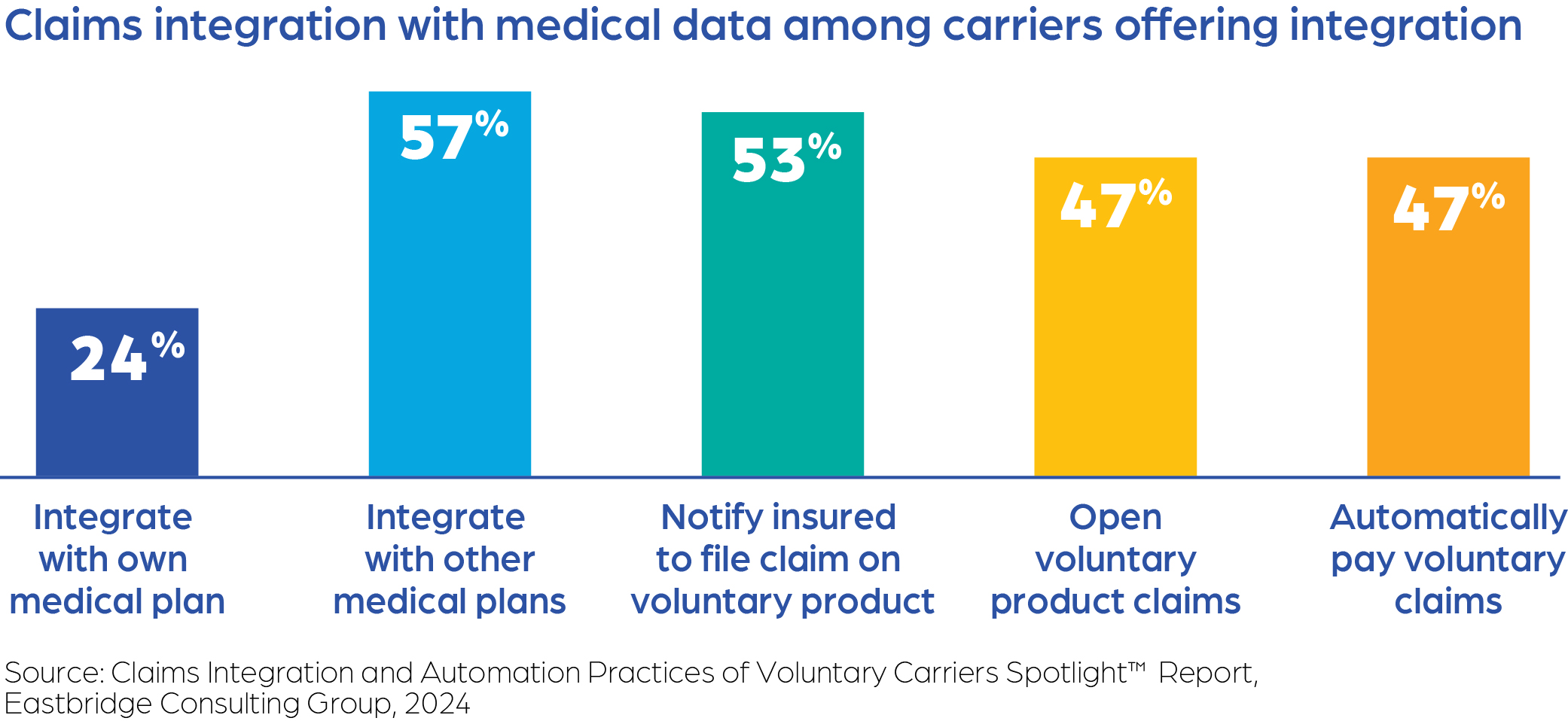

Claims integration is another fast-growing trend with expanding capabilities. Research shows more than two-thirds of voluntary carriers offer some type of claims integration service.4 While the approach carriers take to provide this service varies, the majority of carriers offering claims integration will notify employees they should consider filing a voluntary claim, and nearly half automatically pay a voluntary claim for employees. Most carriers provide these services without an additional charge.

Aligning employer and broker needs

Brokers who want to help clients create the most effective — and most affordable — benefits package may need to beware of a tipping point. Carriers surveyed for Eastbridge’s Product Trends report1 say their biggest challenges include balancing the demand for richer benefits with overall profitability and the need for affordable and simpler, easier-to-understand products. Benefits communication remains essential for a successful offering, but access to employees is a growing concern with the trend toward online self-enrollment. As this trend continues, employers and even brokers may need better education about the value of voluntary benefits and how an impactful communication process is a vital part of the offering.

Outstanding service that offers robust support for brokers, employers and their employees is increasingly recognized as a crucial and valuable asset in a competitive market. 5Star Life’s dedication to making this collaborative experience productive and rewarding sets us apart. Discover more about 5Star Life Insurance Company, our commitment to partnering with you, and our award-winning service recognized by Forbes two years in a row by visiting us at 5starlifeinsurance.com.

1 Voluntary Products Trends Frontline™ Report, Eastbridge Consulting Group, February 2024

2 MarketVision™—The Employer Viewpoint© Report, Eastbridge Consulting Group, February 2024

3 Voluntary Whole and Universal Life Products” Spotlight™ Report, Eastbridge Consulting Group, 2025

4 Claims Integration and Automation Practices of Voluntary Carriers Spotlight™ Report, Eastbridge Consulting Group, 2024

Empowering Brokers

Stay ahead of the curve! Sign up below to receive our exclusive Thought Leadership Series articles and gain the latest insights and expert tips. Don’t miss out — click the link to explore even more valuable content that can elevate your knowledge.